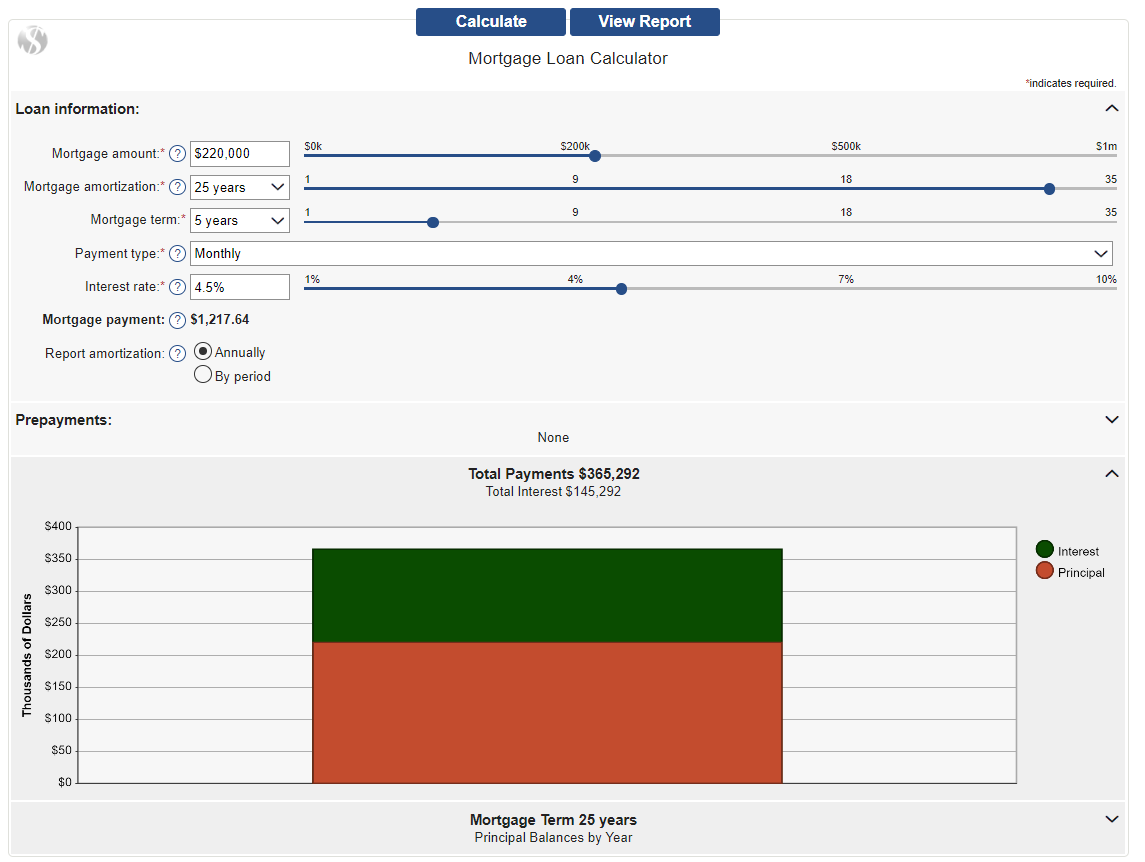

Mortgage amount

Original or expected balance for your mortgage.

Interest rate

Annual interest rate for this mortgage.

Amortization period

The number of years over which you will repay this loan. The most common mortgage amortization periods are 20 years and 25 years.

Mortgage payment

Your principal and interest payment (PI) per period.

Payment type

The payment type determines the frequency of payments. Monthly will have 12 payments per year, weekly 52, bi-weekly 26 and bi-monthly 24.

Accelerated weekly and accelerated bi-weekly payment options are calculated by taking a monthly payment schedule and assuming only four weeks in a month. We calculate an accelerated weekly payment, for example, by taking your normal monthly payment and dividing it by four. Since you pay 52 weekly payments, by the end of a year you have paid the equivalent of one extra monthly payment. This additional amount accelerates your loan payoff by going directly against your loan’s principal. The effect can save you thousands in interest and take years off of your mortgage.

The accelerated bi-weekly payment is calculated by dividing your monthly payment by two. You then make 26 bi-weekly payments. Just like the accelerated weekly payments you are in effect paying an additional monthly payment per year.

Total payments

Total of all monthly payments over the full term of the mortgage. This total payment amount assumes that there are no prepayments of principal.

Total interest

Total of all interest paid over the full term of the mortgage. This total interest amount assumes that there are no prepayments of principal.

Prepayment type

The frequency of prepayment. The options are none, weekly, bi-weekly, semi-monthly, monthly, yearly and one-time payment.

Prepayment amount

Amount that will be prepaid on your mortgage. This amount will be applied to the mortgage principal balance, based on the prepayment type.

Start with payment

This is the payment number that your prepayments will begin with. For a one-time payment, this is the payment number that the single prepayment will be included in. All prepayments of principal are assumed to be received by your lender in time to be included in the following month’s interest calculation. If you choose to prepay with a one-time payment for payment number zero, the prepayment is assumed to happen before the first payment of the loan.

Savings

Total amount of interest you will save by prepaying your mortgage.

Report amortization

Choose how the report will display your payment schedule. Annually will summarize payments and balances by year. Monthly will show every payment for the entire term.